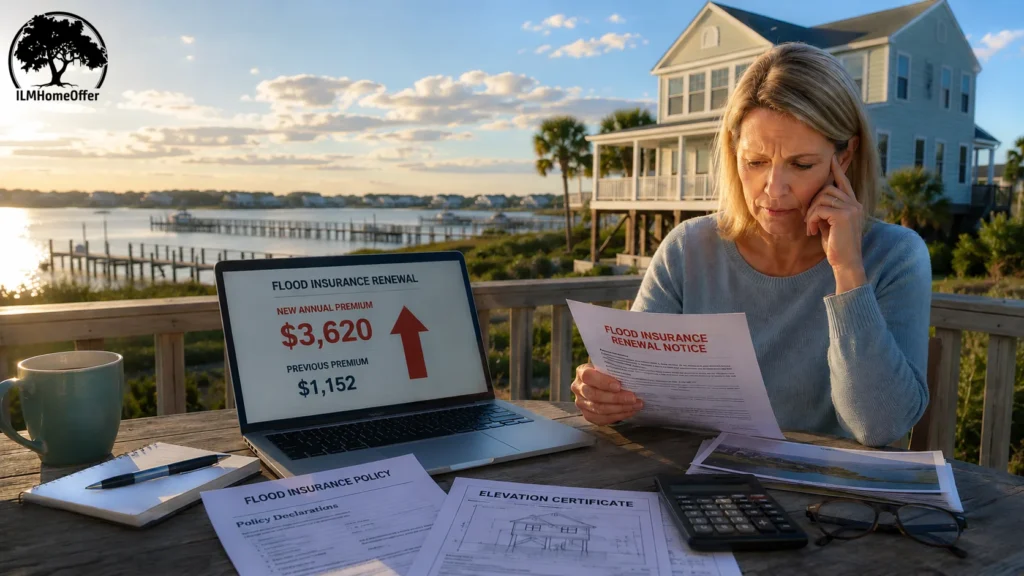

Are rising flood insurance premiums making your Wilmington home harder to sell?

You’re not alone. Selling a coastal NC home with rising flood insurance is one of the most common challenges in the Wilmington market right now. Higher premiums affect buyer qualification and deal structure, but sellers who price thoughtfully, disclose clearly, and understand their options still close quickly and confidently. Here’s exactly how to do it.

Rising flood insurance premiums are quietly reshaping how buyers approach coastal properties in Wilmington and across southeastern North Carolina. Higher monthly costs affect a buyer’s mortgage qualification, the pool of eligible buyers, and the timeline to close. That doesn’t mean homes in flood zones won’t sell — it means sellers who price with insurance in mind, disclose clearly, and time the sale strategically can still move quickly and with confidence.

Selling a coastal NC home with rising flood insurance is about preparation and transparency — not panic. The right approach keeps serious buyers engaged and deals on track.

How Rising Flood Insurance Premiums Change the Game When Selling a Coastal NC Home

Rising flood insurance premiums change the sale dynamic by tightening the budget math for buyers. Higher premiums reduce the monthly payment a borrower can tolerate, which narrows the pool of qualified buyers and influences financing terms. A buyer who could have qualified for a larger loan may now face a smaller maximum loan amount once premium costs are factored in.

This shifts the importance of pricing, disclosures, and timing of insurance quotes early in the process. In the Wilmington market, many properties near waterways still find buyers who value location and mitigation steps — as long as the numbers on paper make sense. Being transparent about current premiums and policy status helps buyers and lenders move from interest to a firm offer faster.

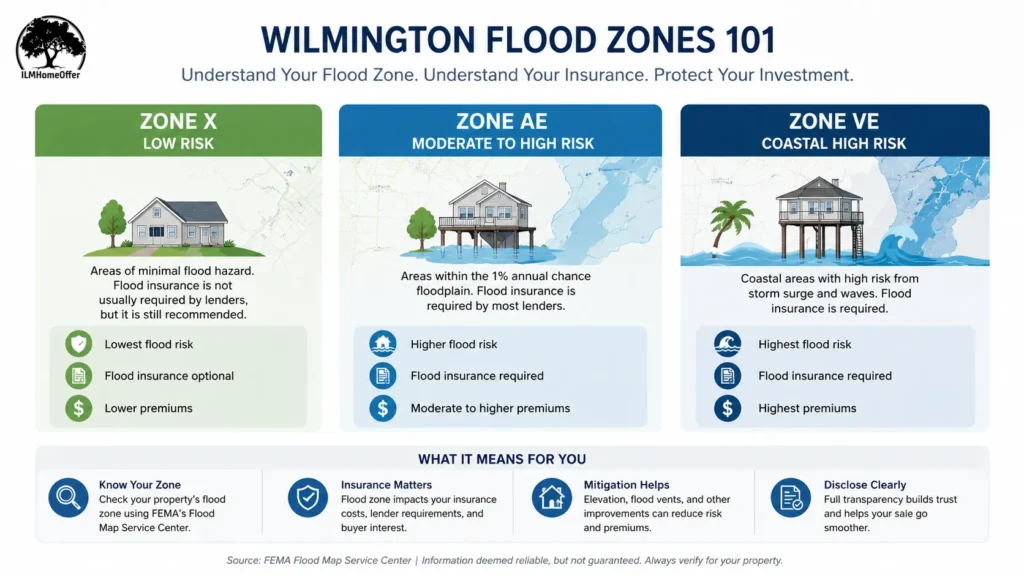

Wilmington Flood Zones 101: How Local Risk Designations Affect Price and Buyer Interest

In Wilmington, flood zone designations determine who can borrow and at what cost — which directly shapes price expectations and buyer interest. The most relevant categories are high-risk zones (AE and VE) and lower-risk zones (Zone X). Lenders tailor their requirements to these designations, and properties in higher-risk zones typically prompt more buyer questions about premiums, coverage, and mitigation.

On the ground, expect more questions about elevation, past flooding, and any mitigation work completed. Always verify your flood zone designation using official FEMA flood map tools before listing, and be transparent with buyers about what those designations mean for insurance quotes and lender requirements.

Proximity to waterways and local storm histories can subtly influence buyer perception even when the home has solid mitigation features. Knowledge of your zone going in is the single most useful preparation step.

What Wilmington Buyers and Their Lenders Look for in Flood Insurance

Buyers and lenders in Wilmington focus on clear visibility into flood risk and the cost of coverage. They typically want to know:

- Current flood zone designation

- Whether flood insurance is in place and the approximate annual premium

- Type of coverage — NFIP vs private insurer

- Any elevation-related documentation or certificates

Understanding the difference between NFIP vs private flood insurance can help you answer buyer questions confidently and reduce back-and-forth during underwriting. Sharing a current policy declarations page, a premium estimate, and elevation-related documentation upfront can meaningfully speed up the path to a firm offer.

When a seller is open about insurance costs and potential mitigations, it eases negotiations and reduces last-minute surprises — which is the most common reason coastal NC deals fall apart late in the process.

Pricing a Coastal NC Home as Flood Insurance Costs Rise

Pricing in a market with rising flood insurance means thinking about total monthly housing costs, not just sale price. A thoughtful approach can position the property attractively even when the annual premium is high. Start with local comps that factor in flood-zone status — not just sale price — and look at days-on-market and price reductions in both flood-zone and non-flood-zone neighborhoods.

Practical pricing tactics include:

- Starting with a price that reflects the insurance reality rather than ignoring it

- Offering a first-year premium credit to reduce the buyer’s upfront burden

- Structuring concessions that address insurance costs specifically

If storm damage is also a factor in your property’s condition, understanding how that affects value and repair costs is an important part of pricing correctly.

Flood Disclosures, Documents, and Negotiation Leverage in North Carolina

North Carolina requires sellers to disclose known flood risks and material facts about flood damage. Having key documents ready shortens the path to a clean underwriting review:

- Elevation certificate if available

- Current flood policy declarations page (redact sensitive personal information)

- Any engineering or mitigation reports

- Claims history relevant to flood events

Disclosures reduce uncertainty for buyers and lenders and prevent delays from last-minute document requests. In negotiations, ready access to accurate flood information supports smoother conversations about price adjustments or credits tied to insurance costs. If you’re unsure what must be disclosed, consult a licensed NC real estate professional or attorney.

For context on how closing timelines work in North Carolina and what to expect at each stage of the process, it’s worth reviewing what a typical NC sale looks like from contract to close.

Timing Your Sale Around Flood Insurance and Policy Changes

Timing matters in North Carolina because policy renewals, NFIP updates, and local underwriting practices influence when a buyer can close. If insurance costs are expected to shift significantly, listing when premium estimates are stable helps buyers finalize financing without delays.

Build in extra diligence periods to obtain fresh quotes, align lender timelines, and coordinate a flexible closing date. Cash buyers can shorten timelines further since they aren’t bound by lender-driven insurance requirements — though each buyer path has its own tradeoffs. If you have a preferred move timeline, map it into your listing strategy and disclosures so buyers can plan accordingly.

Elevation Certificates, Premiums, and Resale Value in Wilmington

An elevation certificate is a document prepared by a licensed professional that details a property’s elevation relative to base flood height, the flood zone designation, and the building’s lowest habitable floor. This certificate helps insurers and lenders refine how they rate risk — and in some cases can support meaningfully lower premiums if the home sits higher than the flood map assumes.

For sellers, an elevation certificate can improve buyer confidence and reduce post-offer delays caused by underwriting questions. The cost and timing of obtaining one varies, but for a high-value coastal property in a flood-prone area, the potential premium savings and deal-acceleration benefits often justify the effort before listing.

When a Cash Buyer Makes More Sense Than a Traditional Listing

In markets where flood insurance costs are rising, a cash-offer path provides speed and certainty that many financed buyers can’t match. A local cash buyer can close with fewer contingencies related to financing and insurance — translating into a shorter, more predictable timeline.

Three scenarios where a cash path often wins when selling a coastal NC home with rising flood insurance:

- You need to move quickly due to personal timing or ongoing premium increases

- The property needs significant repairs that could complicate lender financing

- You value certainty and a clean as-is close over chasing a premium price with contingencies

The tradeoff is that cash offers may come in below the top of the market — so compare a few options and weigh your timeline and risk tolerance before deciding. ILM Home Offer is a local cash buyer serving southeastern NC that can close in as little as 7 days on as-is properties.

If the property has been sitting vacant, there are additional considerations around liability and carrying costs worth understanding before you list or accept an offer.

Step-by-Step Plan for Selling a Wilmington Coastal Home Despite Rising Flood Insurance

Here is a practical checklist from now through closing:

- Confirm your property’s official flood zone using FEMA’s flood map service

- Gather current insurance information and obtain a few premium quotes to share with potential buyers

- Gather elevation-related documents or determine whether you need an elevation certificate

- Talk with a local real estate professional about pricing with flood costs in mind

- Prepare a disclosure packet covering known flood risks, mitigation steps, and claims history

- Decide whether to list traditionally or explore a cash-offer path based on your timeline

- Build in insurance-related credits or concessions if premiums are expected to rise

- If pursuing a cash offer, compare several offers and verify proof of funds

- Align closing timing with insurance and lender readiness to minimize coverage gaps

- Close on your preferred terms

Frequently Asked Questions

Is it hard to sell a home in a flood zone in Wilmington, NC?

Selling a coastal NC home with rising flood insurance involves extra steps, but many Wilmington properties sell well when pricing, disclosures, and documentation are handled clearly. The key is preparation — not avoidance.

Can you get flood insurance on a coastal beach house in NC?

Yes. Flood insurance is available through the National Flood Insurance Program (NFIP) or private insurers. Cost and availability depend on flood zone, elevation, and other risk factors. Buyers should work with a licensed insurance professional to get accurate quotes before committing.

Should I hurry to sell my coastal NC property before flood insurance costs rise further?

There isn’t a single right answer. Rising premiums can create urgency for some owners, but decisions should balance market conditions, personal timelines, and exit options — including cash offers that can reduce risk without requiring a rushed or discounted listing.

What is an elevation certificate and do I need one to sell?

An elevation certificate documents your home’s elevation relative to base flood height. It’s not legally required to sell, but it can lower premiums, speed up underwriting, and improve buyer confidence — making it worth obtaining for most coastal properties in higher-risk zones.

Ready to Sell Your Coastal NC Home?

Selling a coastal NC home with rising flood insurance is absolutely possible with the right information and preparation. Price with insurance in mind, disclose clearly, get your documents in order, and match your exit path to your timeline.

If you want a faster, as-is option without repairs, showings, or insurance contingencies, ILM Home Offer buys coastal NC properties for cash and can close in as little as 7 days. Visit ilmhomeoffer.com for a no-pressure, no-obligation conversation about your property.